Despite a gloomy economic backdrop, the fintech revolution is pushing on. Numerous transformative fintech trends in 2022 are propelling adoption in the $332.5 billion financial technology industry, even in the face of global inflation, a “crypto winter,” and sour geopolitical sentiments.

As of 2021, over 90% of US citizens use some kind of fintech service, and there will be an estimated 2 billion global users of the fintech industry by the end of 2022. This mass global adoption is projected to reach a lightning-fast growth rate of 19.8%, per Vantage Market Research, supported by increasing fintech customer acquisition, investment and collaboration.

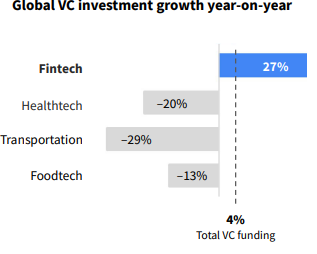

Indeed, the fintech market has been attracting sustained venture capital investment – even amid a general plunge in the venture capital space. With a 27% year-on-year increase in VC investment in 2022, exceeding the average of 4% significantly, the industry has proven to be resilient as it further emerges, according to a report from Dealroom, an Amsterdam-based provider of startup data.

Venture Capital Investments in 2022, Fintech Q1 2022 Report

This effervescence being witnessed in the fintech industry is strongly linked to its innovation and responsiveness to consumer needs.

Understanding the fintech trends that are propelling emerging innovations and improving customer experience, thus, will help to explain just how this industry has managed to continue growth in such turbulent times.

Top fintech trends in 2022 to be on the outlook for

What emerging fintech trends should companies explore in 2022?

We spoke with a group of fintech founders, CEO and executives around the world to take the pulse of what is happening on the ground.

1. Finance becomes smarter with robotic process automation, artificial intelligence and machine learning

More processes in the fintech and financial services ecosystem are increasingly automated, thus increasing speed and efficiency as tasks are executed by rule-based software robots or more complex and responsive algorithms.

Robotic Process Automation (RPA) has replicated manual human activities to implement repetitive tasks. Today, work such as generating reports, streamlining claims, managing financial information and more are increasingly executed through RPA technology. According to Juniper Research, revenue from using RPA will increase by a whopping 400% between 2018 to 2023.

Moreover, machine learning (ML), a subset of artificial intelligence (AI), is increasingly enabling fintechs to automate higher-level tasks. With machine learning, algorithms can be now programmed to “learn and adapt” to certain actions and inputs and develop better responses over time.

There is lots of potential being – and yet to be made – with this tech. According to McKinsey, AI can deliver incremental value of up to $1 trillion each year if harnessed with success.

In 2022, ML and AI is being deployed in multiple facets of the fintech sector, including cybersecurity, customer service (chatbots), biometrics, record and transaction processing, financial advisory (robo advisors) and business development.

ML and AI can also be particularly useful for cashflow management, which will, according to Petr Macek, CEO of Caflou, a business management system, become an increasing priority as “the CEOs of many more companies start looking for a solution to manage their cashflow, and not only on the top-company level but also on lower levels, like the project level.”

2. Digital payments become expansive and more inclusive

The digital payment industry is one of fintech’s largest segments and its growth is one of the biggest fintech trends to watch today, especially since its pandemic-instigated 2020 surge has now led to continued adoption in 2022.

The segment grew for two reasons: firstly, more customers switched to contactless and digital payments to execute transactions during the pandemic; and secondly, more businesses adopted digital payment upon recognizing it as an enabler of long-term growth.

With many businesses embarking on digitization, digital payments have evolved as a critical contributor to growth. Businesses are thus increasingly adopting digital payment processors to facilitate increasing demand for online and convenient transactions whilst offering a seamless customer experience.

Similarly, more consumers have continued to embrace digital payments.

The mobile payments industry first reached $1.54 trillion in 2020 and it increased by 27.9% to $1.97 trillion in 2021. The market is projected to continue this rapid growth at a rate of 29.1% annually till 2028, by which time it would be worth an estimated $11.83 trillion.

Amid this rapid growth, contactless payments stands out as one of the biggest drivers of the sector.

Contactless payments were already on an uptrend before exploding in usage during the pandemic. Enabled by Near-Field Communication Technology, customers pay by just moving their phones near to payment terminals.

Meanwhile, for e-commerce customers, new developments in digital wallets and QR codes have supported growth in this industry, propelling e-retail sales in excess of $4.2 trillion in 2022 (to date).

Another innovation driving the payments sector is so-called request to pay/request for payments technology (RPT). In essence, RPT enables merchants and businesses to directly request bill payments from customers and other businesses.

Requests for payments are sent to the payers billing address, and they can then accept or decline the request without compromising personal details. This particular fintech trend has been more widely spreading across Europe, India and America in 2022, with banks and fintech startups increasingly leveraging the technology.

[Want to better enable payment collection for utility businesses? Read this article about bill payment aggregators to learn more.]

3. Companies are expanding their services with embedded finance

Businesses are now transcending the offer of simply providing digital payments. With embedded finance, non-financial businesses can now offer financial services that personalize and enhance the customers experience.

Embedded finance allows businesses to integrate financial services into nonfinancial products as add-ons. One of the biggest use cases of embedded finance is Buy Now, Pay Later (BNPL).

BNPL allows customers to pay for a product or service in multiple installments. It can also allow a customer to purchase extra products and services and pay for it as a more convenient time.

Amazon, for instance, offers insurance for products bought on the store, thus eliminating the need to contact an insurance agent.

Zama Ndlovu, Head of Corporate Communications and Marketing at MFS Africa, a platform enabling mobile payments and remittances in Africa, believes that the ongoing growth in the Buy Now, Pay Later space is helping merchants to “bolster their conversion rates” by offering “last minute loans for cash poor consumers”.

Commenting on this particular fintech trend, he stated that B2B leaders, Point of Sale (POS) vendors and e-commerce providers should wake up to the promise of instant credit in the B2B marketplace. In this way, more platforms can capture value by helping customers “split purchases across multiple payments”.

Valued at $54.3 billion, according to Future Market Insights, the embedded finance market is estimated to grow to a jarring $99 billion by 2026.

[Looking to build add-on payment services? Reloadly offes plug-and-play APIs for sending gift cards, airtime top-ups and data bundles without the need to sign up for any contract. Get in touch with our customer support to learn more.]

4. Companies are creating security and financial systems on the blockchain

More companies are contemplating that without the blockchain promise of “internet of the future”, the architecture of their fintech platform will not be robust enough to meet evolving consumer needs and outperform competitors.

Thus, companies are increasingly exploring the future of blockchain technology and Web 3, which promises tamper-proof security and financial infrastructure via decentralized finance (DeFi), as well as a support for myriad of other emerging trends such as digital assets (such as NFTs), cryptocurrencies and the metaverse.

First, blockchain technology, as a distributed database, provides a higher level of security by enabling immutable, tamper-proof transactions. With stringent requirements for access to transaction data, fintechs can make their systems more immune to cyber attacks

Blockchain technology also helps to disintermediate payments and build greater.

Thus, consumers can execute transactions between themselves without an active intermediary. This works by enabling certain protocols that are set to be triggered by trading consumers, and only then allowing the transaction to be automatically executed. With that, fintech companies can facilitate P2P trading and lending between customers and other businesses.

“Blockchain-backed supply chain financing plays a critical role in forecasting business stability,” says Anna Kogan, CEO of Ficus, a fintech dedicated to making lending easier by helping SMEs overcome common problems with small business loans. “Not only can a buyer follow the money flow in real-time, but the added layers of trust and transparency can also decrease interest rate burdens.”

Secondly, tokenization, cryptocurrencies and NFTs open up opportunities for fintech to target an expanding market of enthusiasts who want to acquire and exchange digital assets.

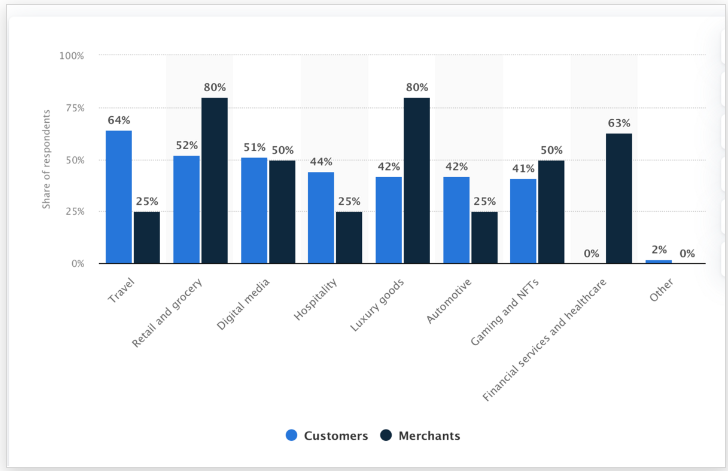

As crypto adoption increases, according to Chain Analysis, more businesses are becoming willing to accept crypto payments .

Willingness to use/accept cryptocurrencies for payments by consumers/merchants across various industries worldwide as of 2021 (Statista)

5. Banking becomes more digital via open APIs

More people are banking online, instigating legacy banks to offer more digital and mobile banking services alongside neobanks and online-only banks.

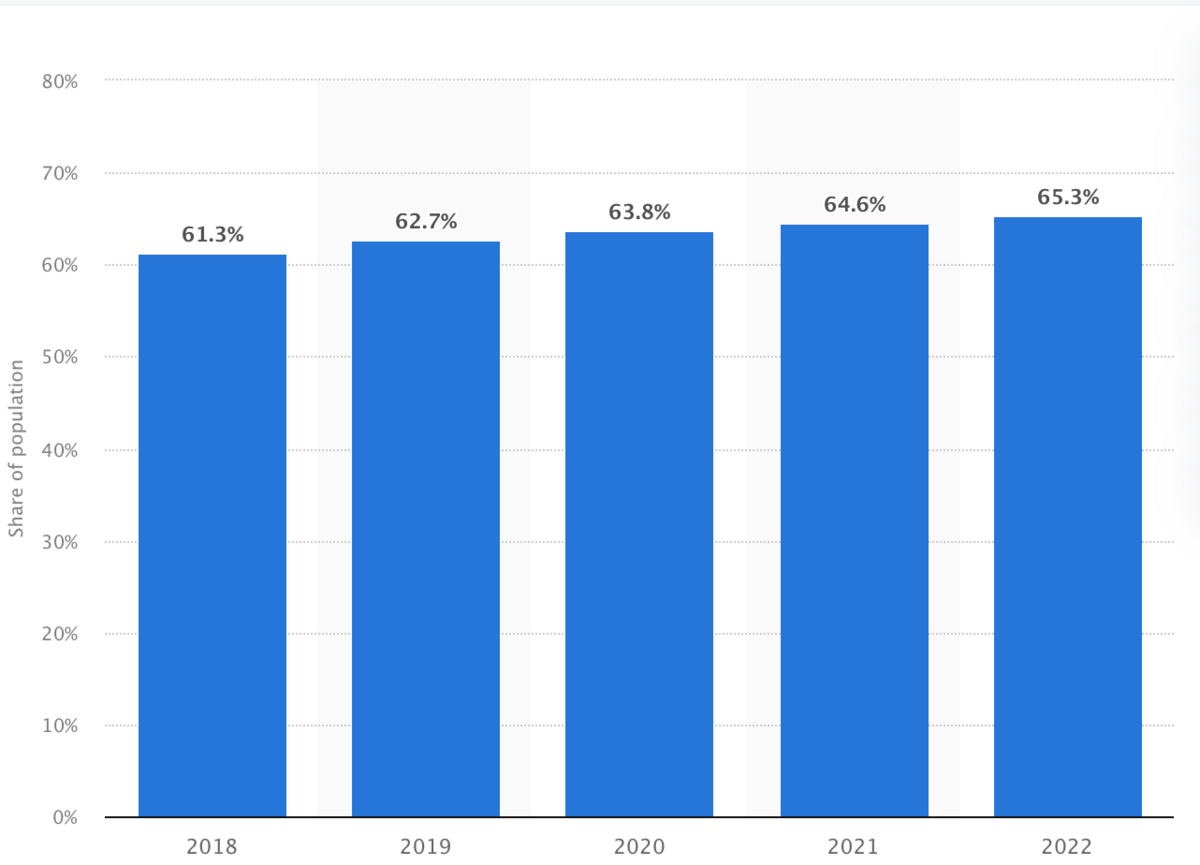

According to Statista, 63% of bank customers in the United States transact online in 2022.

Share of population using digital banking in the United States from 2018 to 2022 (Statista)

Digital banking services help traditional banks and fintechs better cater to customers who want to conveniently bank from their smartphones and via the internet. Additionally, it helps reduce the overhead costs of running a business, such as rent, electricity and more, thus creating a cost-effective means to run banking.

In fact, many banks have closed physical branches and made concerted efforts to strengthen their digital presence as a result of the rise of digital banking.

Additionally, digital banking aids the delivery of personalized services via chatbots, robo-advisors, budgeting apps and more.

“Whoever owns the experience wins”, according to Chris Scislowicz, North America Credit Lead of Accenture, and digital payment methods are better able to enable the delivery of financial services to millennials and Gen Z through apps, social media, virtual credit cards and more.

Open banking and banking-as-a-service (BaaS) are innovative fintech trends that continue to transform the sector into 2022 as well.

First, BaaS is helping banks generate more revenue by charging fees for the use of their payment infrastructure by fintechs, as fintechs still continue to rely on traditional banking infrastructure to build financial products.

Also, open banking has created unprecedented access for fintechs and non-banks to customer data when certain parameters are met (designed to ensure the privacy and protection of the customer). Access to data, as well as the use of banking infrastructure, has aided the delivery of innovative, tailor-made services to customers, along with collaboration between banks and fintechs.

The connective tissue putting all of this together is Application Programming Interfaces (APIs).

APIs are “a software intermediary that allows two applications to talk to each other”, according to Mulesoft, and they are enabling a new world of access for fintechs to customer data and banking payment infrastructure.

This interaction between banks, financial companies and fintech startups is helping both parties leverage on each other’s assets. Chris Dean, CEO of Treasury Prime advises that, “if you’re a fintech and you want to move money, you need to partner with a well-run bank. Fintechs are friends to banks, not foe.”

As a whole, the open API technology movement, which is used in banking among many other industries, is worth an estimated $2.48 billion and will grow at a CAGR of 24.81% to a projected price tag of $14 billion by 2030, according to Verified Market Research.

[APIs are accelerating innovation across many industries, including e-commerce, banking and telecommunications. Read “The APIs Accelerating Innovative Across Industries” to learn more.]

6. Concerted efforts are being made to increase financial inclusion

Financial inclusion is recognised for its importance by both public agencies, private entities and financial institutions across the world, and it is one of the top fintech trends of 2022.

Featured in eight of the United Nations Sustainable Development Goals, financial inclusion is featured at the forefront of many innovative fintech visions, with many fintech startups being created solely to try and ensure that more people can equitably access payments, remittances, loans and more investment opportunities.

The Covid-19 pandemic was also a catalyst for the expansion of financial inclusion, according to the 2021 Global Findex database. According to the database, 71% of people worldwide now have a bank or mobile account in 2021, up dramatically from 51% in 2011.

However, there are still about 1.4 billion people worldwide who remain unbanked, according to the World Bank.

Over the past year, more fintech platforms have been increasingly looking to expand services to areas that are predominantly excluded, and they will continue to need to rely on financial literacy and education to drive penetration.

7. Fintech regulations become more stringent

As more fintech trends emerge, so does regulation grow to adapt to protect customers and regulate business activities in the space.

Fintech regulation needs to adapt because each innovation brings new challenges, and with privacy issues and cybercrime prevalent in the financial services space, protecting users is a top priority for governments.

Fintech businesses must thus ensure that they continue to invest in compliance professionals to protect customers, gain user trust and avoid the consequences of flouting laws.

Moreover, fintech businesses are also increasingly investing in regulatory technology (known as regtech) to ensure they remain up to date with compliance and regulations.

Final thoughts

With these numerous transformative fintech trends emerging in 2022, financial and non-financial businesses must work harder if they want to adequately retain and win customers.

To maintain a competitive edge in a rapidly evolving market, businesses should take these trends as a guide to learn where to best invest in acquiring new tech, talent and partnerships to help them sustain growth.

[Looking to expand your capabilities and stay atop fintech trends in digital payment APIs? Reloadly’s customer support team is readily available to help guide you.]